Member News

Member Blogs

Member Offers

🚗 Quarter 3 Offers Now Live at Northampton Audi! ⚡

🎄 Christmas Countdown Continues at Kents Hill Park 🎄

HarisSolutions Launches April 40% Discount on Training Courses to Boost Professional Growth

news article

LIMITED TIME OFFER: 40% OFF ALL TRAINING COURSES

33.7 Million working days lost to job related health issues or injuries in the past year

Latest News

Charity support

Sponsors Needed For Our a Touch of Red Gala Ball

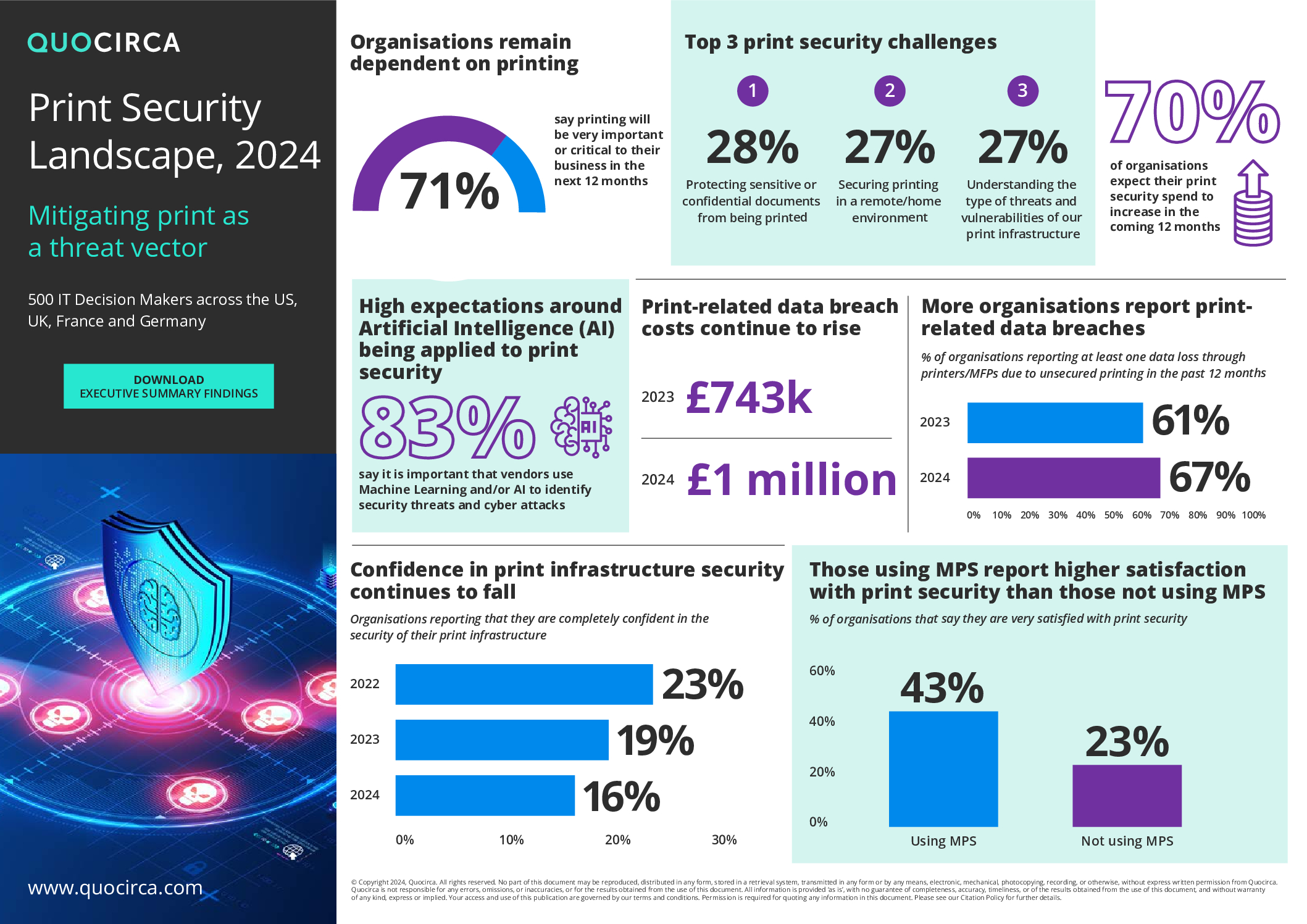

Is Your Business Missing Out on a Game Changing Print Strategy?

Kents Hill Park Unveils Exclusive ‘Pick & Mix’ Offer for Event Organisers

Kents Hill Park Unveils Exclusive ‘Pick & Mix’ Offer for Event Organisers

")